Why Active Investing Works in Sri Lanka’s Frontier Market

By ACP Insights

Updated Dec 3, 2025 5:59 pm ET

Vibrant market street bustling with shoppers and colorful signs.

COLOMBO, October 2025

As Sri Lanka’s capital markets recover from years of macro stress, a clear divide has re-emerged between active and passive investment strategies. Recent performance data suggest that the country’s equity dispersion, combined with improving fundamentals, may offer one of the most compelling active-management opportunities in Asia’s frontier universe.

Macro Recovery: From Crisis to Credibility

Sri Lanka’s post-crisis recovery continues to surprise even seasoned observers. GDP grew around 5 % in 2024, while inflation has stabilized in the 5–6 % range after peaking above 50 % two years ago. The Central Bank of Sri Lanka, backed by a US $ 2.9 billion IMF program, has regained policy credibility with a unified rate near 8 %.

At the same time, foreign reserves have rebuilt to roughly US $ 6 billion, the rupee has steadied, and debt restructuring has reduced future servicing costs by more than half. For professional allocators, these shifts mean one thing: a collapsing risk premium — and the potential for earnings re-rating in equities still trading at single-digit P/E multiples.

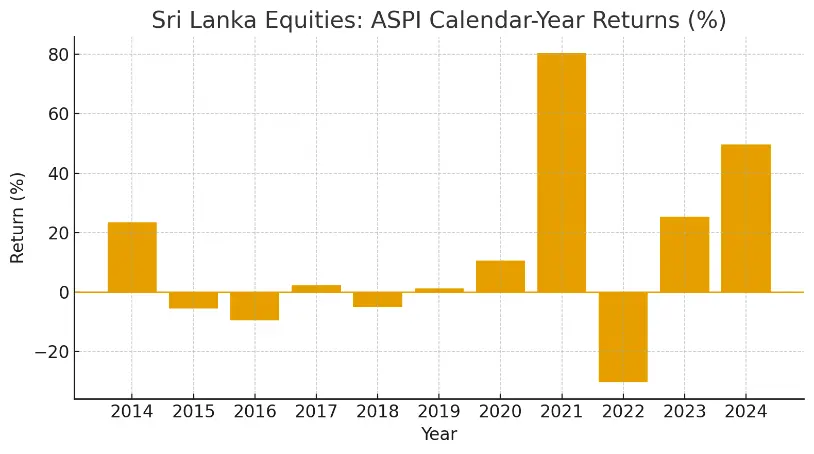

Chart A - Sri Lanka Equities: ASPI Calendar-Year Returns (%) (2014 – 2024, LKR basis)

High dispersion years such as 2021 (+ 80.5 %) and 2024 (+ 49.7 %) illustrate the opportunity set for tactical, active management.

Active vs Passive: The Frontier Dispersion

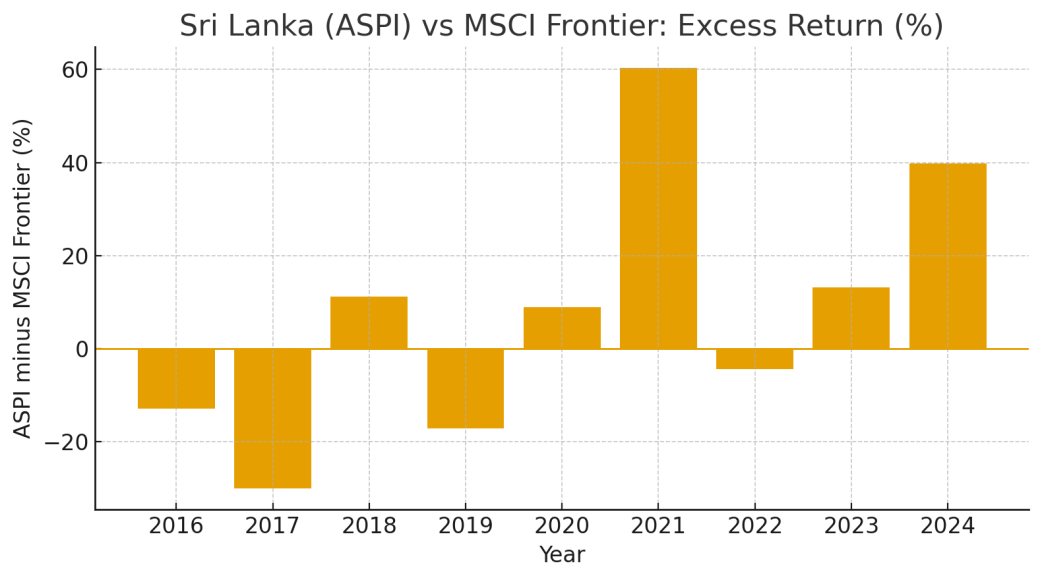

Chart B – ASPI vs MSCI Frontier: Excess Return (%) (2016 – 2024, directional comparison LKR vs USD)

In global emerging markets, active management historically outperforms when dispersion between countries widens — and Sri Lanka exemplifies that pattern. Over the past decade, its market returns have swung from − 30 % to + 80 %, while index weights under-represent sectors driving domestic growth such as banks, materials, and renewable infrastructure.

The Colombo All-Share Price Index (ASPI) outperformed the MSCI Frontier Markets Index by roughly 60 percentage points in 2021 and 40 points in 2024, yet lagged in mid-cycle years. That volatility, rather than discouraging investment, highlights the inefficiency that active managers exploit — through research depth, liquidity timing, and selective exposure.

Why Active Works in Sri Lanka

1 Country Allocation Matters

Macroeconomic reform, fiscal consolidation, and monetary independence all shift sector leadership. Active country allocation allows managers to overweight banking and consumer names during credit recoveries or tilt toward exporters when currency stabilises — advantages a passive vehicle cannot capture.

2 Stock Selection Drives Alpha

Sri Lanka remains under-covered: fewer than 20 companies receive consistent research coverage. Active investors can identify mis-priced assets early, especially as corporate governance standards improve and foreign participation returns. The local market’s inefficiency is a structural source of information alpha.

3 Portfolio Construction Flexibility

Core active strategies can manage liquidity risk dynamically — reducing exposure when daily turnover compresses, or expanding into mid-caps when breadth improves. The capacity to vary active share through the cycle is vital in a market where annual dispersion can exceed 100 percentage points.

4 Governance and Engagement

Beyond stock picking, engagement is alpha-additive. Companies with improving ESG and governance profiles often see valuation multiple expansion; active managers can accelerate this process through direct dialogue and stewardship.

5 Market Inefficiency Premium

The inefficiency premium — the spread between intrinsic and market value — remains wide in Sri Lanka. As data quality, digitalization, and liquidity deepen, that premium narrows, rewarding early professional capital that entered through active mandates.

The Strategic Case for Active Exposure

For professional investors, a blended approach remains prudent:

Core active sleeve: benchmark-aware, style-neutral, focused on liquidity and valuation cycles.

Passive overlay: provides cost-efficient exposure but limited alpha.

Frontier satellite: captures dispersion-driven opportunities, ideally through regulated vehicles (UCITS, AMCs, or managed accounts).

Historical evidence suggests that active risk budgets of 3–5 % and investment horizons of 3–5 years align best with Sri Lanka’s re-rating cycle.

Looking Ahead: 2025 and Beyond

If GDP growth sustains near 4–5 %, inflation remains anchored, and debt restructuring continues, Sri Lanka could re-enter global frontier indices with a market capitalization uplift of over 30 %. The correlation between earnings upgrades and foreign inflows remains strong, implying that active allocators will once again set the tone for price discovery.

Bottom Line

In an environment defined by reform momentum, valuation gaps, and limited passive coverage, Sri Lanka stands as a textbook case for active management. For investors seeking frontier alpha, the opportunity is not in broad exposure — it’s in precision.

Data sources: Reuters, FT, MSCI Frontier Markets, Colombo Stock Exchange, Central Bank of Sri Lanka (2024–25). Past performance is not indicative of future results.