- Nov 8, 2025

- 6 Comments

- ACP Insight

- Photo of Colombo Port, Sri Lanka

Key Takeaways |

- Global markets are transitioning toward slower growth and tighter liquidity, reinforcing a return to fundamentals over momentum.

- Dispersion has widened, increasing the importance of selectivity rather than broad market exposure.

- Capital is becoming more disciplined, favouring reform visibility, policy credibility, and valuation support.

- Elevated concentration in consensus trades heightens portfolio risk, strengthening the case for diversification.

- Valuation gaps across emerging and frontier markets remain structurally attractive within a selective framework.

Global markets rarely shift direction all at once. The more common pattern visible now, is a gradual change of texture: growth moderates, liquidity tightens, dominant narratives reach saturation, and investors begin to reassess where genuine value still resides. The past year has carried exactly that tone: not crisis, not exuberance, but a return to fundamentals.

In that environment, smaller markets with clear reform anchors and improving macro stability are quietly returning to institutional conversations—not as speculative ideas, but as part of broader diversification thinking.

Sri Lanka’s trajectory sits within this transition.

Inflation eased, policy settings stabilised, and volatility declined. As those pressures receded, equity risk premia compressed and valuations adjusted accordingly.

A Slowdown with Structure, Not Panic

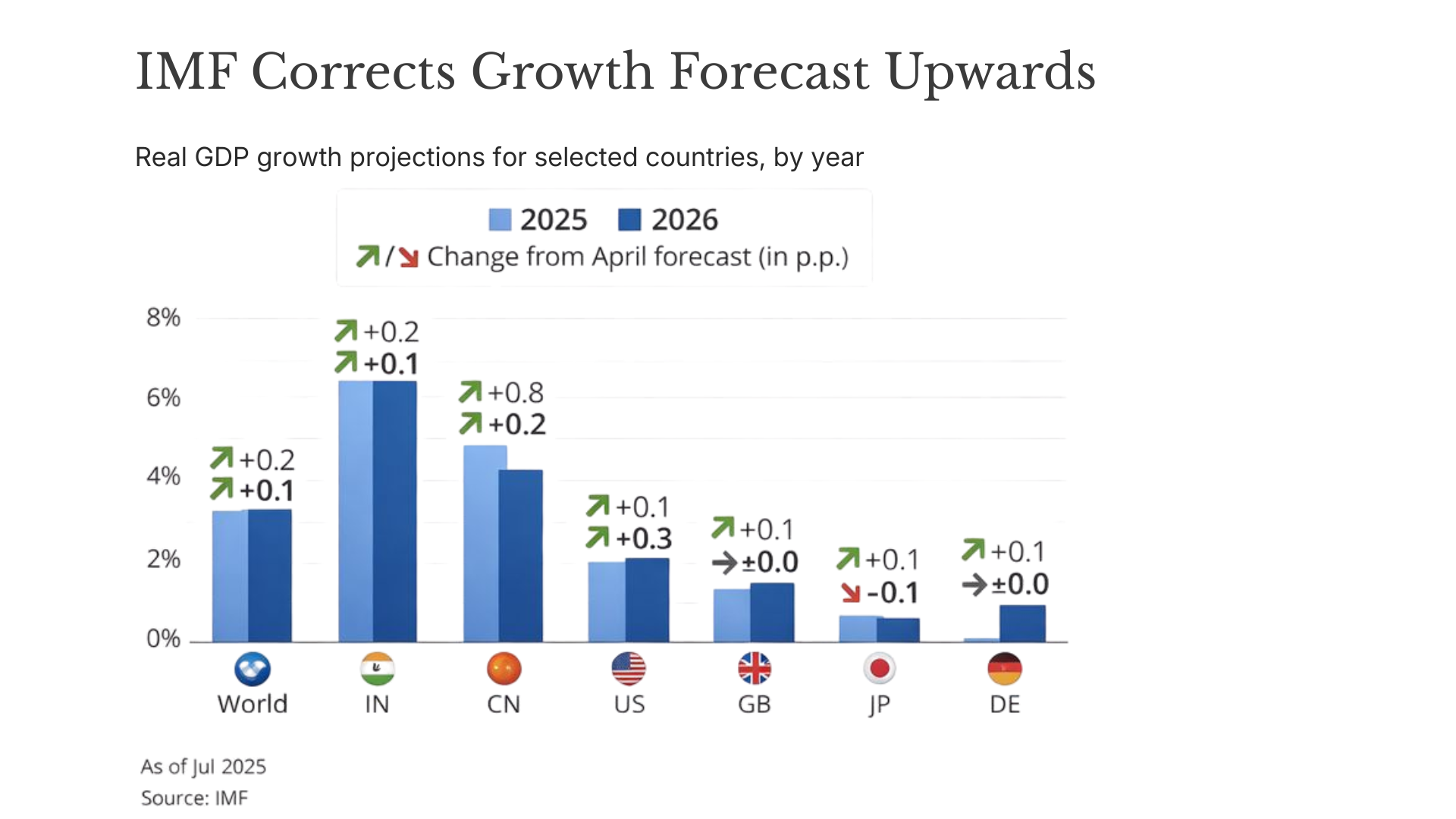

The IMF’s latest projections show the world expanding at a measured pace: 3.2% in 2025 and 3.1% in 2026. Advanced economies run near 1.5%, while emerging and frontier markets maintain a structurally higher rhythm above 4%.

For investors, the takeaway is straightforward: global growth is slower, but dispersion still exists—and dispersion is where alpha is built.

Moderation has shifted attention from momentum-driven trades toward markets where valuation, reform, and long-term positioning matter more than short-term sentiment.

The Investment Pipeline Tightens - and Clarifies

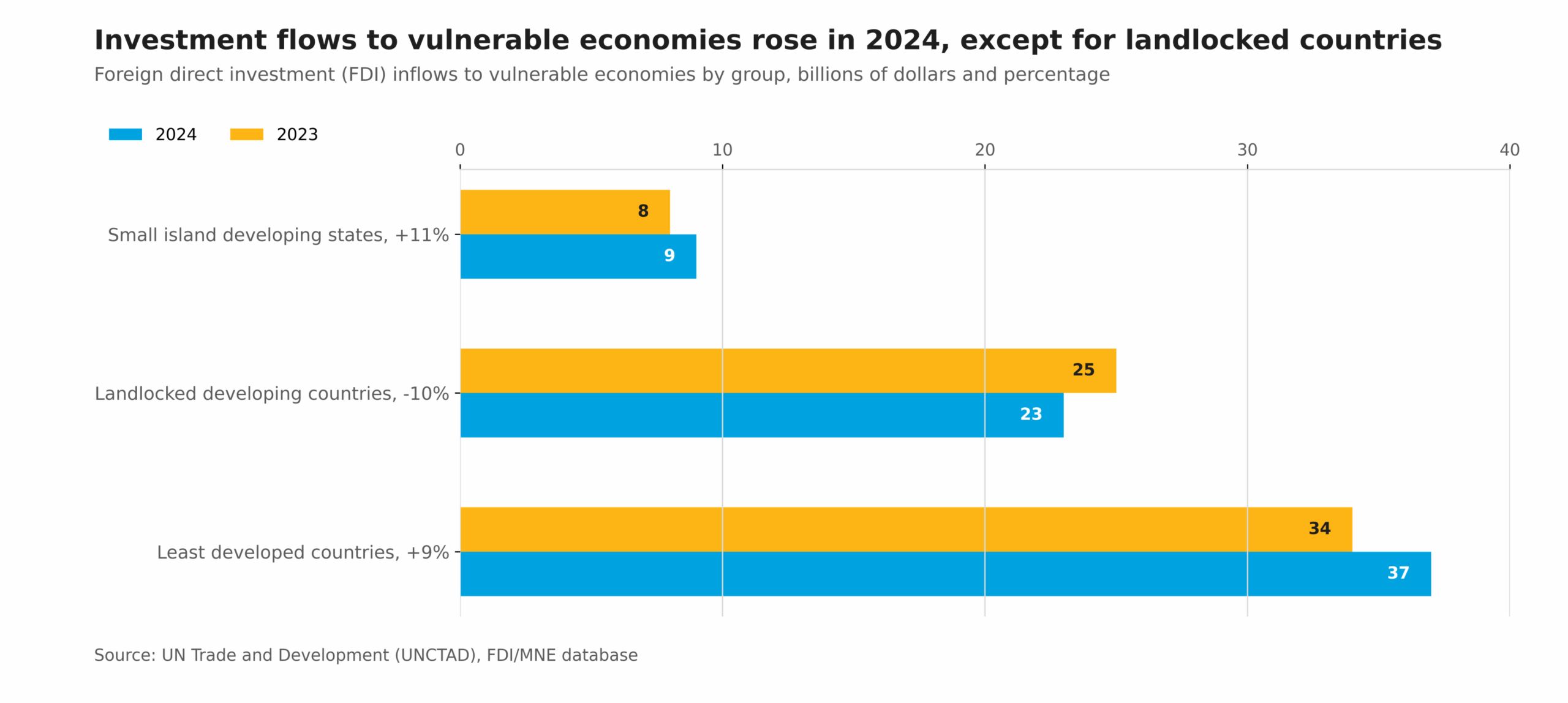

According to UNCTAD, global FDI flows fell 3% in H1 2025, while industrial and infrastructure project announcements saw double-digit declines. Capital is not retreating, but re-calibrating. Large markets absorb the slowdown; selective markets benefit from sharper evaluation.

The shift is meaningful: as global investment becomes more selective, it rewards markets where policy direction is clearer and valuation still compensates for risk.

The Limits of Consensus: AI, Concentration, and Re-pricing Risk

AI and U.S. mega-cap technology continue to dominate global equity flows. Yet institutional surveys show a rising concern about concentration risk: over half of managers now believe AI-linked equities may be overextended

Crypto’s sharp drawdown earlier this year only reinforces the broader theme—when too much capital crowds into the same stories, the marginal return weakens.

Fragmentation and FX Trends Reshape the Playing Field

Tariff risks, geopolitical tensions, and supply-chain diversification continue to disrupt established trade corridors. IMF modelling suggests renewed tariff escalations could subtract more than a percentage point from global growth.

Meanwhile, the U.S. dollar’s softening introduces new return asymmetries for non-USD markets.

Small economies located along emerging regional corridors—South Asia, the Middle East, East Africa—are benefitting not from size, but from position.

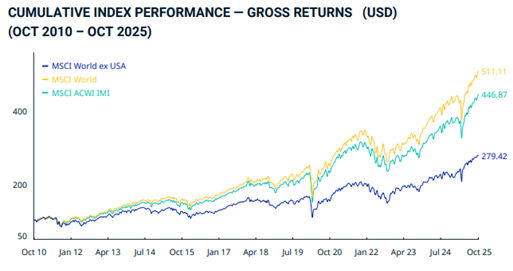

A Valuation Reset Across Emerging and Frontier Markets

From a pure valuation perspective, emerging and frontier equities continue to trade at attractive discounts versus developed markets.

World Bank projections of further commodity price declines through 2026 support net-importing economies, improving fiscal dynamics.

UNCTAD data shows divergence within developing markets—Asia stabilized, while other regions weakened—highlighting the importance of selectivity.

For investors who have lived through multiple cycles, the current setup will feel familiar: dispersion is back, valuation gaps have reopened, and fundamentals matter again.

Institutional Positioning: Confident but Narrow

BofA’s survey shows global cash levels at 3.7%, below the 4% line often seen as a “sell signal.” Equities are overweight globally, and risk sentiment leans optimistic despite persistent tail risks.

When positioning compresses, diversification through less-owned exposures becomes a practical risk management tool—not a contrarian statement.

Sri Lanka: A Market Emerging From Adjustment

Sri Lanka’s story aligns with what sophisticated investors watch in frontier markets:

A reform framework anchored by the IMF

Improving external balances and reserve positions

A sustained rebound in tourism and remittances

Fiscal consolidation and tighter monetary governance

A strategic location in a rapidly integrating regional corridor

This is not about “high beta” or speculative optimism.

It is about structural repair following a deep adjustment cycle—something veteran investors recognize immediately.

Structured Access: UCITS and Listed Certificates

For investors evaluating smaller markets, access matters as much as the macro case.

European-regulated UCITS structures provide daily NAV publication, oversight, and transparency. They serve as one recognized pathway through which certain investors—subject to jurisdictional rules and individual suitability—can gain exposure. The Sri Lanka Opportunity Fund (UCITS) operates within this UCITS framework.

Listed certificates, including Active Management Certificates (AMCs) on the Vienna Stock Exchange, offer daily pricing and a rule-based methodology, aligning with global settlement standards. They provide another regulated mechanism through which exposure may be evaluated.

These structures do not imply suitability or preference—they simply create organized, regulated channels through which investors can assess a market undergoing structural change.

Conclusion: A Cycle Turning Back Toward Fundamentals

The global environment is not defined by crisis or acceleration but by nuance.

As themes like AI and U.S. mega-cap technology absorb most flows, underlying concentration risk grows.

As FDI normalizes and valuations reset, structural reform stories regain relevance.

As currencies and supply chains shift, geography returns to the discussion.

Sri Lanka sits within these intersections.

UCITS-regulated structures and listed certificates provide frameworks through which exposure can be evaluated—not as a recommendation, but as part of an institutional discussion about diversification, valuation, and frontier recovery.

For investors who have lived through multiple cycles, the contours of this moment feel familiar.

The rotation may be quiet, but it has begun.