- Dec 8, 2025

- 6 Comments

- ACP Insight

- Treaty on European Union signed in Maastricht – archive, 1992 | European Union

Key Takeaways |

- Global pension CIOs allocate for durability across decades, prioritising governance, resilience and long-term compounding over short-term narratives.

- Frontier exposure is evaluated at the total-portfolio level, with emphasis on correlations, stress behaviour and contribution to long-horizon objectives.

- Successful frontier allocations are precisely sized, using disciplined sleeves that protect portfolio stability while allowing compounding to work.

- Multiple engines of return matter — growth, income, inflation protection and diversification must operate together within a coherent structure.

- Frontier markets reward long-cycle patience, where reform, stabilisation and valuation reset unfold over years, not quarters.

A Chief Investment Officer in a global pension fund lives with a quiet burden that few outside the room ever understand. Their decisions echo across decades. They allocate not for applause, but for the retired teacher in 2045, the factory worker in 2050, the child who will one day grow into a beneficiary they will never meet. They operate in a world where errors compound slowly, where bravery must be quiet, and where the only true currency is judgment earned through cycles.

This is why CIOs think differently.

They sit at the crossroads of mathematics and mortality, at the intersection of markets and human promises. They do not chase excitement. They pursue durability. They do not hunt for the loudest opportunities. They search for the ones that survive storms. Their portfolios must stand through inflation regimes, political shocks, liquidity deserts and whispered crises that never make the news.

And in this long horizon vigilance, CIOs discover a pattern. Some of the most enduring opportunities emerge not in crowded markets but in places where capital has fled, where reforms have begun quietly, and where assets trade at discounts that reflect fear rather than fundamentals. Frontier markets often live in this quiet intersection between mispricing and renewal.

The following lessons blend philosophy with practice. They reflect how global pension CIOs navigate uncertainty, identify resilient allocations and integrate frontier exposure into disciplined portfolio construction.

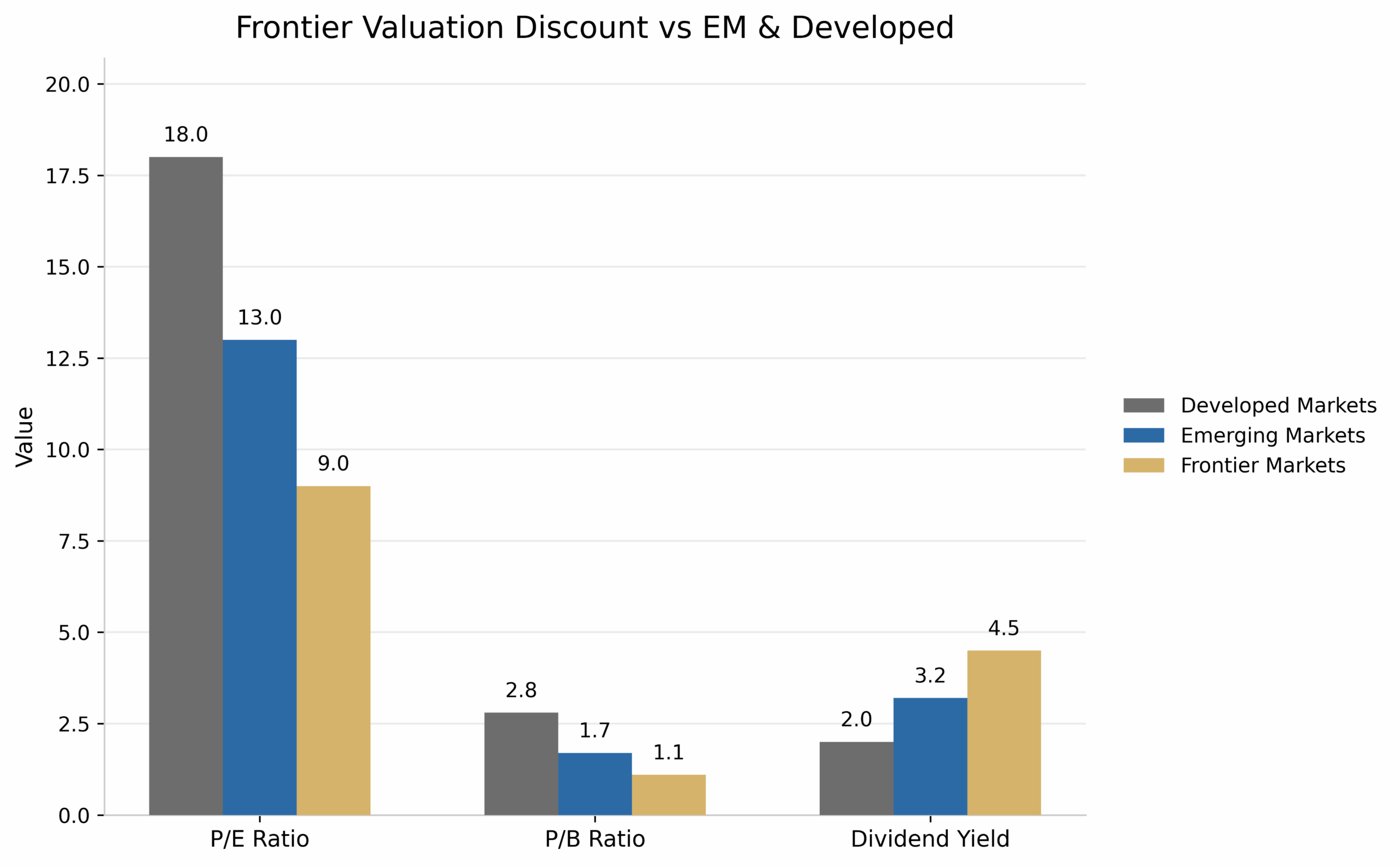

In that environment, smaller markets with clear reform anchors and improving macro stability are quietly returning to institutional conversations—not as speculative ideas, but as part of broader diversification thinking.

Sri Lanka’s trajectory sits within this transition.

Inflation eased, policy settings stabilised, and volatility declined. As those pressures receded, equity risk premia compressed and valuations adjusted accordingly.

Lesson 1: Begin with the total portfolio, not the country narrative

A CIO never begins with a country pitch. They begin with a portfolio question:

“If I add this exposure, does the entire structure become stronger or weaker in a crisis?”

They do not evaluate frontier markets in isolation. They examine cross correlations, stress behavior and return drivers. When the Government Pension Fund of Japan evaluated emerging exposures, it studied whether the allocation reduced reliance on domestic deflation cycles and improved long term return stability.

A country story may inspire interest, but the portfolio story determines approval.

Lesson 2: Reverse engineer decisions from long horizon objectives

CIOs work backwards from time.

They begin with actuarial demands, real return targets, demographic forecasts and liquidity thresholds. Only then do they consider which markets or strategies can support these obligations.

Norway’s NBIM, for example, incorporated emerging exposures after concluding that long term demographic shifts and global income convergence would lift global equity weights over time. It was not a trade. It was a structural response to the world that was coming.

Frontier markets fit when they support long horizon outcomes rather than short term speculation.

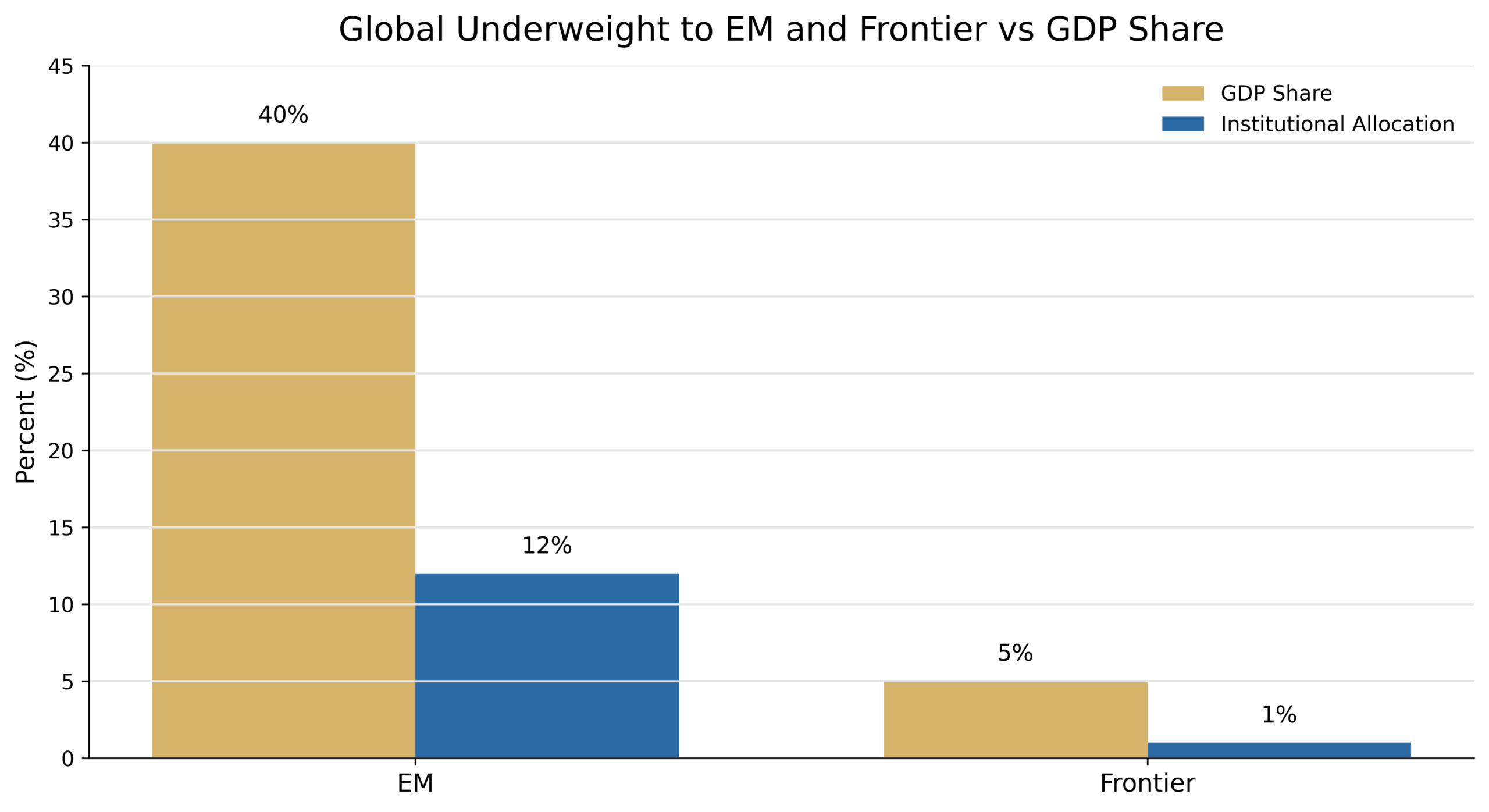

Lesson 3: Size with precision and restraint

To a CIO, sizing is destiny.

Most frontier allocations fail not because the thesis is wrong, but because the sizing is careless.

Institutional sizing is deliberate. A frontier sleeve between two percent and five percent is not caution.

It is discipline. It preserves stability while allowing long term compounding to do its quiet work.

CIOs know that a well-placed small allocation held over time is more powerful than a large allocation held inconsistently.

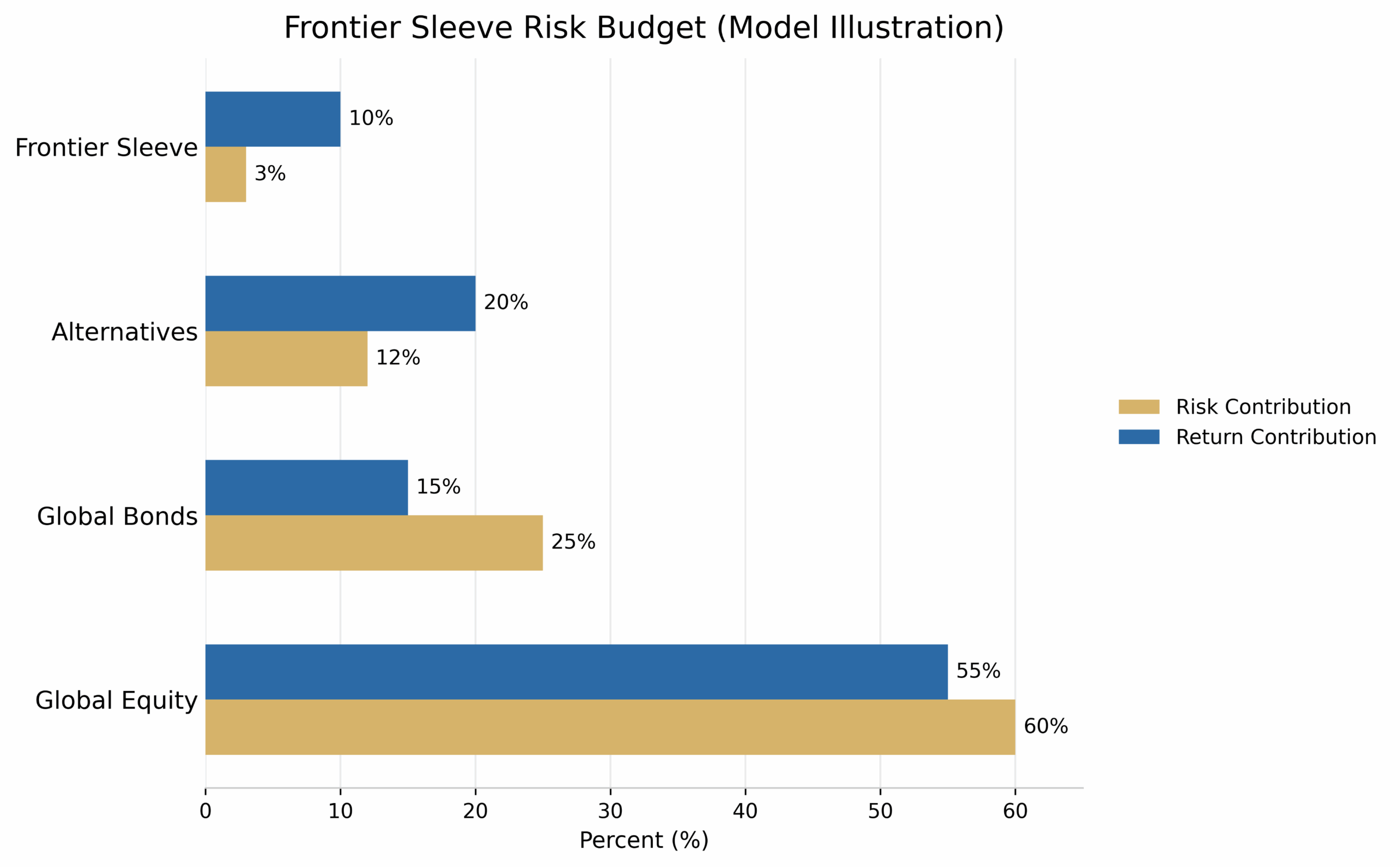

Lesson 4: Blend multiple engines of return

CIOs do not rely on one source of performance. They assemble portfolios like architects.

· Growth that expands capital.

· Income that stabilises volatility.

· Inflation hedges that preserve purchasing power.

· Diversifiers that respond differently when global patterns break.

Frontier markets can offer all four characteristics.

During macro reform cycles, earnings accelerate, real yields remain elevated and currencies often move from over adjustment to recovery. CIOs integrate these elements not as isolated opportunities but as part of a long term structural blend.

This combination transforms frontier exposure from a risky edge into a thoughtful component of global return construction.

Lesson 5: Governance and liquidity are preconditions for allocation.

Before a CIO studies anything else, they examine structure.

· Is custody segregated.

· Is valuation transparent.

· Is dealing frequency predictable.

· Is liquidity robust in stressed conditions.

Japan’s GPIF refuses any exposure that does not meet strict operational and reporting standards. Not because these markets are unattractive, but because governance failures create permanent risk that cannot be diversified.

Frontier markets earn institutional trust only when access structures are clean, transparent and regulated.

Lesson 6: Recognise that frontier markets are long cycle commitments

CIOs do not enter structural themes with short term expectations. They understand that frontier markets behave like multi year narratives rather than quarterly trades.

The most powerful frontier cycles historically followed similar sequences.

A policy reset.

A stabilisation period.

A valuation compression.

A gradual recovery supported by improving fundamentals.

Long term allocators thrive in this sequence because they allow the full cycle to play out rather than reacting to early volatility.

Lesson 7: Communicate allocation purpose with clarity and discipline

CIOs must justify decisions to boards, regulators and beneficiaries. This requires simplicity with depth.

Why this allocation exists.

What role it plays.

How it behaves in stress.

How it strengthens the total portfolio.

How it is governed.

How it aligns with long term objectives.

A frontier sleeve becomes institutionally legitimate only when it can be explained in terms that are repeatable, measurable and aligned with fiduciary duty.

Clarity builds trust.

Trust builds durability.

Durability builds long term return.

Conclusion: What CIOs truly teach us

The greatest lesson from global pension CIOs is not a tactic. It is a worldview.

They design the portfolio before they choose the product.

They think in decades rather than seasons.

They act with patience where others act with urgency.

They value resilience over novelty.

They respect the quiet power of compounding.

They understand that markets reward those who endure uncertainty, not those who escape it.

When frontier markets are viewed through this lens, they undergo a transformation.

They are no longer seen as volatile outliers.

They become strategic footholds.

They become mispriced opportunities shaped by reform, valuation reset and long cycle renewal.

Frontier markets do not need to shout. They simply need to be understood through the eyes of those who invest for the future, not for the moment.

A Quiet Note on Access for Institutional Allocators

For investors who require regulated structures to express a frontier allocation, ACP provides a UCITS V fund and an Actively Managed Certificate focused on Sri Lankan assets. These vehicles follow established European governance and reporting standards, allowing allocators to integrate frontier exposure through familiar institutional frameworks.

(This reference is factual, non-promotional and compliant. No performance is quoted. No call to action is stated.)