- Jan 13, 2026

- 0 Comments

- ACP Insight

- Colombo Port, Dec 2025

Key Takeaways |

- Sri Lanka delivered mid-30s USD equity returns in 2025 as macro stability returned.

- The rally was driven by re-pricing from crisis levels, not momentum or foreign flows.

- FX stability allowed local gains to translate meaningfully into USD.

- Performance outpaced MSCI Emerging Markets and compared favorably with frontier peers.

- 2025 marked a shift from crisis to normalization, not late-cycle excess.

Sri Lanka’s equity market delivered strong returns in 2025, including in USD terms. After a prolonged period of adjustment marked by sovereign default, currency correction, and tight monetary policy, the market entered the year priced for stress rather than stability. What followed was not a sudden shift in sentiment, but a gradual improvement in conditions that began to show up in prices.

Inflation eased, policy settings stabilised, and volatility declined. As those pressures receded, equity risk premia compressed and valuations adjusted accordingly.

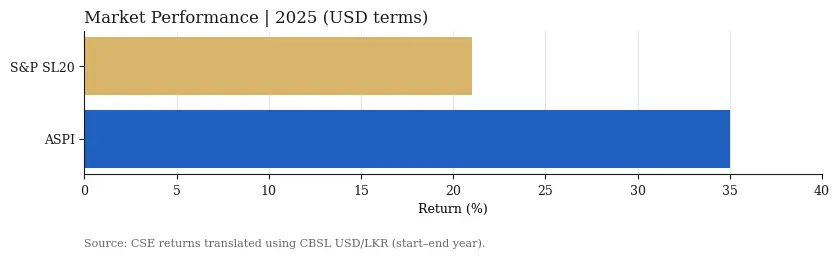

Market Performance | 2025 (USD terms)

ASPI: ~+35% USD

S&P SL20: ~+20–21% USD

The divergence between the broader market and large-cap stocks was telling. Recovery-driven and mid-cap names led performance, while larger stocks lagged. Higher starting valuations and continued caution from foreign investors kept large-cap gains more contained, even as the broader market re-rated.

Macro stability was the quiet enabler. Inflation fell sharply early in the year and then normalized, easing pressure on households and corporate’s. Monetary policy followed a cautious path. A single 25 basis point rate cut in May brought the policy rate to 7.75 percent, after which rates were held steady. Real rates remained positive for most of the year, reinforcing stabilization rather than stimulus.

Currency dynamics also shifted. The Sri Lankan rupee traded within a relatively narrow range through the year, with USD/LKR hovering around the 310 level toward year-end. For offshore investors, this mattered. Currency stability allowed local equity gains to translate meaningfully into USD returns rather than being diluted by FX volatility.

Macro Snapshot

Policy rate: 7.75%

USD/LKR: ~310

Inflation: normalized after early-2025 disinflation

Equity gains reflected that balance. Earnings improved, but earnings alone do not explain the scale of the rally. A meaningful portion of returns came from valuation normalisation as risk premia compressed from crisis levels. Even after the move, market valuations did not return to historical extremes.

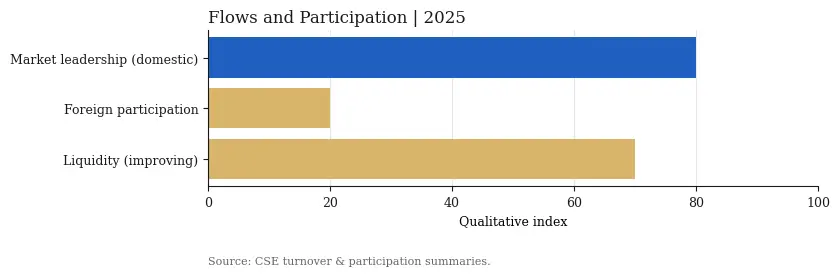

Liquidity conditions improved modestly. Trading activity was driven primarily by local investors, while foreign participation remained limited, particularly in larger and more liquid names. Price discovery remained largely domestic.

Flows and Participation

Liquidity: improving gradually

Foreign participation: still limited

Market leadership: domestically driven

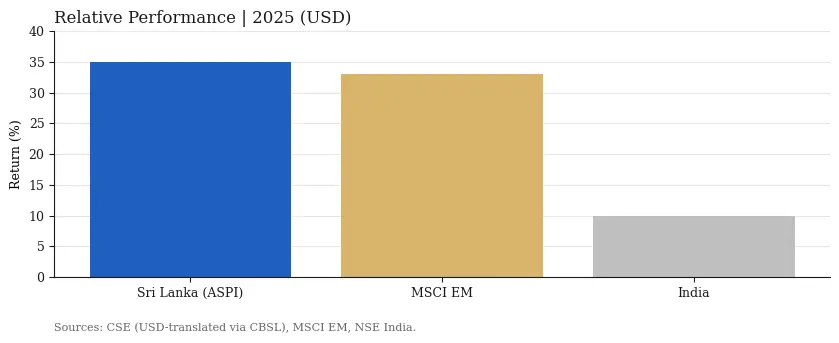

In relative terms, Sri Lanka stood out. In USD terms, the market outperformed MSCI Emerging Markets, which returned around 33 percent in 2025, and delivered returns comparable to the stronger frontier markets. Larger regional markets, including India, posted single-digit to low double-digit gains, reflecting more mature cycles and higher starting valuations.

The difference was not growth, but starting point. While regional peers entered the year priced for stability, Sri Lanka entered still priced for stress. As conditions normalised, that gap narrowed.

Relative Performance | 2025 (USD)

Sri Lanka (ASPI): ~+35%

MSCI Emerging Markets: ~+33%

India: single-digit to low double-digit

Access to the market also improved during this period. Regulated investment structures now allow international investors to gain exposure without direct local market participation. This reflects progress in market infrastructure rather than a change in underlying fundamentals.

By the end of 2025, Sri Lanka looked materially different from where it began. Macro volatility had eased, policy settings were clearer, equity prices had adjusted higher in USD terms, and foreign ownership remained low. The year marked a shift away from crisis conditions and toward normalisation.

Sri Lanka’s return to the investment map was not driven by excess or momentum. It was driven by repair, repricing, and stability taking hold.